When do we need to issue a Bill of Supply?

GST-registered businesses generate tax invoices for buyers. Typically, these invoices state the GST rate - how much GST was charged on the goods and services sold. Even so, certain GST-registered businesses cannot charge any tax on invoices they issue. These dealers need to issue a Bill of Supply. It is issued when GST does not apply to a transaction or when the customer will not be required to reimburse the GST.

Who needs to issue a Bill of Supply?

Here are examples of who needs to issue a Bill of Supply:

Composition Dealer

If the taxpayer's turnover is less than Rs 1.5 crores (Rs 75 lakhs for the north-east states and Uttarakhand), they are eligible for the composition scheme. A dealer using a composition scheme needs to deposit tax on their receipts, and they cannot charge tax to their clients. The composition dealer is responsible for paying GST out of pocket. It is not possible to charge GST on the invoice. The composition dealer, therefore, requires a Bill of Supply in place of a Tax Invoice. On the Bill of Supply, the composition dealer must mention that he is not eligible to collect taxes on supplies.

Exporters

Also, exporters do not have to charge GST on their invoices since export supplies are zero-rated. Thus, a taxpayer exporting goods should generate a Bill of Supply instead of a tax invoice. It must be clearly indicated on the dealer's Bill of Supply that the goods are being exported for IGST payment or under a bond or letter of undertaking without IGST payment.

Exempted Goods Supplier

In order to supply exempt goods or services, a registered dealer must issue a Bill of Supply. For instance, tax invoices are unacceptable when a registered taxpayer provides unprocessed agricultural products.

Contents of Bill of Supply

Here is the information we need to include in the Bill of Supply:

- Supplier's name, address, and GSTIN

- If the buyers are registered, we need to mention their name, address, and GSTIN

- The unique number of Bill of Supply

- Issue Date

- Detail description of goods or services

- The total value of the goods or services

- A signature of the supplier. It can be both digital and paper-based.

- HSN Code of goods or Accounting Code in case of services.

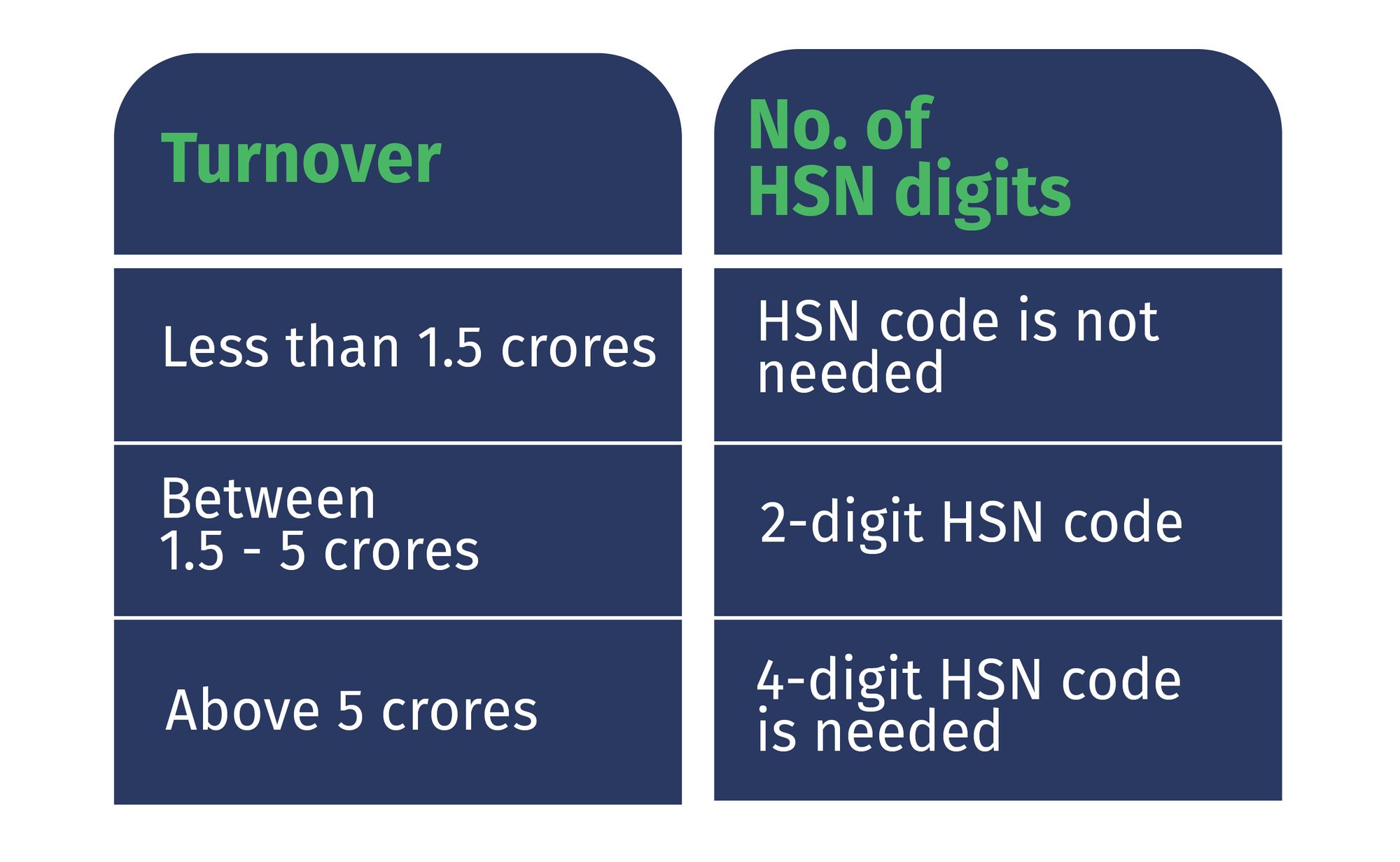

Here are examples of the number of digits that we need to mention according to turnover in the preceding financial year: