Comprehensive Information - What is a GST Tax Invoice? | Meaning, Examples, Templates

What is a GST Tax Invoice and How it Works?

A GST tax invoice is a document that a registered person issues to another registered person for the supply of taxable goods or services. It contains all the relevant information about the transaction, such as the GSTIN of the supplier, the GSTIN of the recipient, the value of the supply, the GST rate, and the amount of GST payable.

Let's see cases when a GST invoice can be either a tax invoice or a bill of supply. A registered supplier for taxable supplies issues a tax invoice. A registered supplier issues a bill of supply for exempt supplies, zero-rated supplies, and supplies to an SEZ unit or an SEZ Developer.

If you want to know more about how gst invoice works in India, read this article.

Types of GST Invoices

Tax Invoice

A tax Invoice under GST acts as a legal document and proof of tax charged. The document is also important for a registered person or company to claim ITC benefits. The document shared acts as a payment term between the seller and the buyer and benefits both equally.

Bill of Supply

The GST section of the law has several clauses that affect the tax chargeable on different sales. Taxes cannot be charged by a supplier of goods and services in some instances. In this case, instead of a Tax Invoice, the seller or buyer must generate a Bill of Supply.

Here are 2 cases in which a Bill of Supply we should issue:

- Suppliers who deal in goods or services that are exempt from GST.

- Rather than using the "Regular Scheme", the GST-registered supplier intends to use the "Composition Scheme".

According to this case, since the buyer is not paying any GST, they will not be able to claim Input Tax Credit. Also, make sure to use the title "Bill of Supply".

Invoice and Bill of Supply (Combined)

Suppliers can sell both, so they are not required to sell GST-applicable products or opt for GST-exempt products. In that case, the GST system of India issues a notification on 24.04.2022. It states that the supplier can generate an invoice that includes all goods and services. A tax invoice and a bill of supply will be combined in this invoice. It is called "Invoice-Cum-Bill-of-Supply" for this reason.

Receipt Voucher

Receipt Vouchers are generated against payments. This serves as proof of payment. This comes into the act when a supplier receives an advance on payment by a buyer. Rather than generating a Tax invoice, a receipt voucher works the best.

Refund Voucher

In some cases, a supplier cannot provide the goods and services ordered by the buyer. If the supplier has already received an advance payment for the supply but fails to fulfil the order, they must issue a refund voucher. The voucher serves as proof of the refund.

Payment Voucher

Suppliers are sometimes not GST registered, but buyers are. In cases where the buyer receives goods and services subject to "Reverse-Charge", the buyer must generate a payment voucher for the supplier.

Want to learn more about the 9 Types of the GST Tax Invoice? This article will help you get detailed information.

Debit and Credit Note

In some cases, the supplier has to supply and simultaneously return some of the payment. In the case of discounts or a sudden decrease in the price of goods or services, this can cause. In the event of a return, the supplier may also be required to refund the amount. The supplier must issue a credit note in such cases. The note will also serve as proof of reduced tax and assist in understanding the variation in chargeable tax. An invoice must be debited if the supplier has mentioned a lower chargeable amount by mistake or in any other circumstance. In other words, this debit is not a token demanding the remainder of the invoice to meet the correct price. In order to maximize the supplier's tax liability, GST debit notes must be shown in the GST return. Registered suppliers generate supplementary tax invoices if they charge the wrong tax amount by mistake. Using an additional tax invoice in the form of a credit or debit note, the tax amount in excess or less can be matched to the correct amount.

How to Create a GST Tax Invoice?

You must have a GST registration number to create a GST Tax Invoice. You will need to mention this registration number on the invoice. The GST registration number must be printed on the invoice legibly.

To create a GST tax invoice, businesses need to have GST-compliant accounting software. The software will generate the invoice and will include all the relevant information required by law.

You can create a GST Tax Invoice using any Kernel software. The software will generate a PDF of the invoice that can be emailed or printed and handed over to the customer.

What are the Mandatory Fields a GST Tax Invoice should have?

A GST tax invoice should contain the information below:

1. Name, address and GSTIN of the provider

2. A unique invoice number

3. Date of invoice

4. Name, address and GSTIN of the beneficiary

5. An explanation of the goods or services supplied

6. The HSN code of the goods or SAC code of the services

7. The volume and cost of the products or services provided

8. The rate of GST charged on the goods or services

9. The absolute worth of the labour and goods provided

10. The amount of CGST, SGST or IGST charged

11. The full amount owed (the sum of GST and the total value of the goods or services)

12. The spot of supply

13. The mark of the provider or an approved agent

Learn more about Mandatory Fields of the GST Tax Invoice here.

How to personalize GST Invoices?

You can personalize your invoices with your company's logo. The Kernel allows you to create and customize GST invoices free of cost.

Who should issue GST Invoice?

GST invoices ought to be issued by businesses that are registered for GST. In most cases, the provider of products or services can issue the GST invoice to the client. However, there are some special cases where the recipient of the products or services could issue the invoice instead.

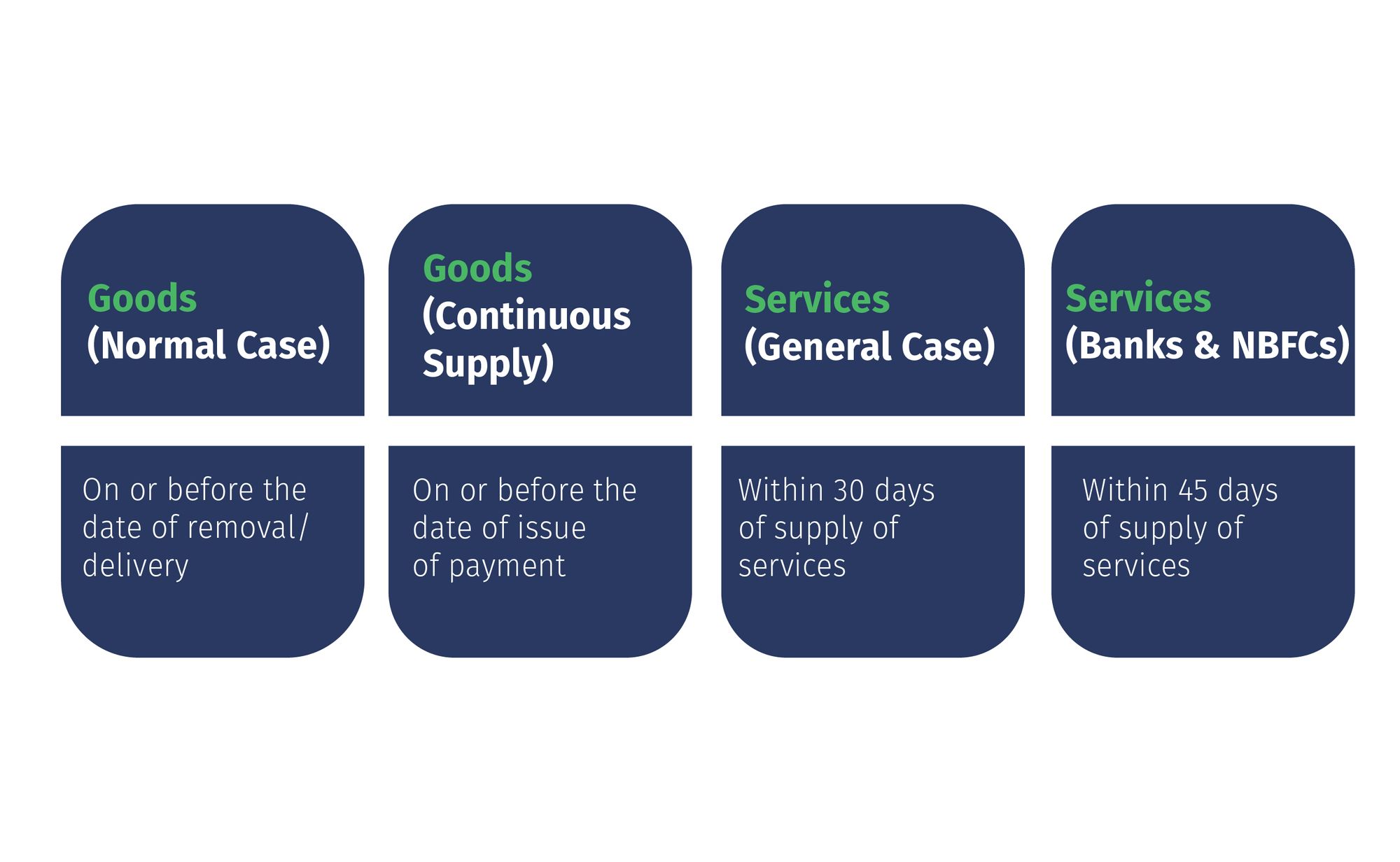

By when should you issue invoices?

Invoices should be issued within 21 days from the date of supply of goods or services.

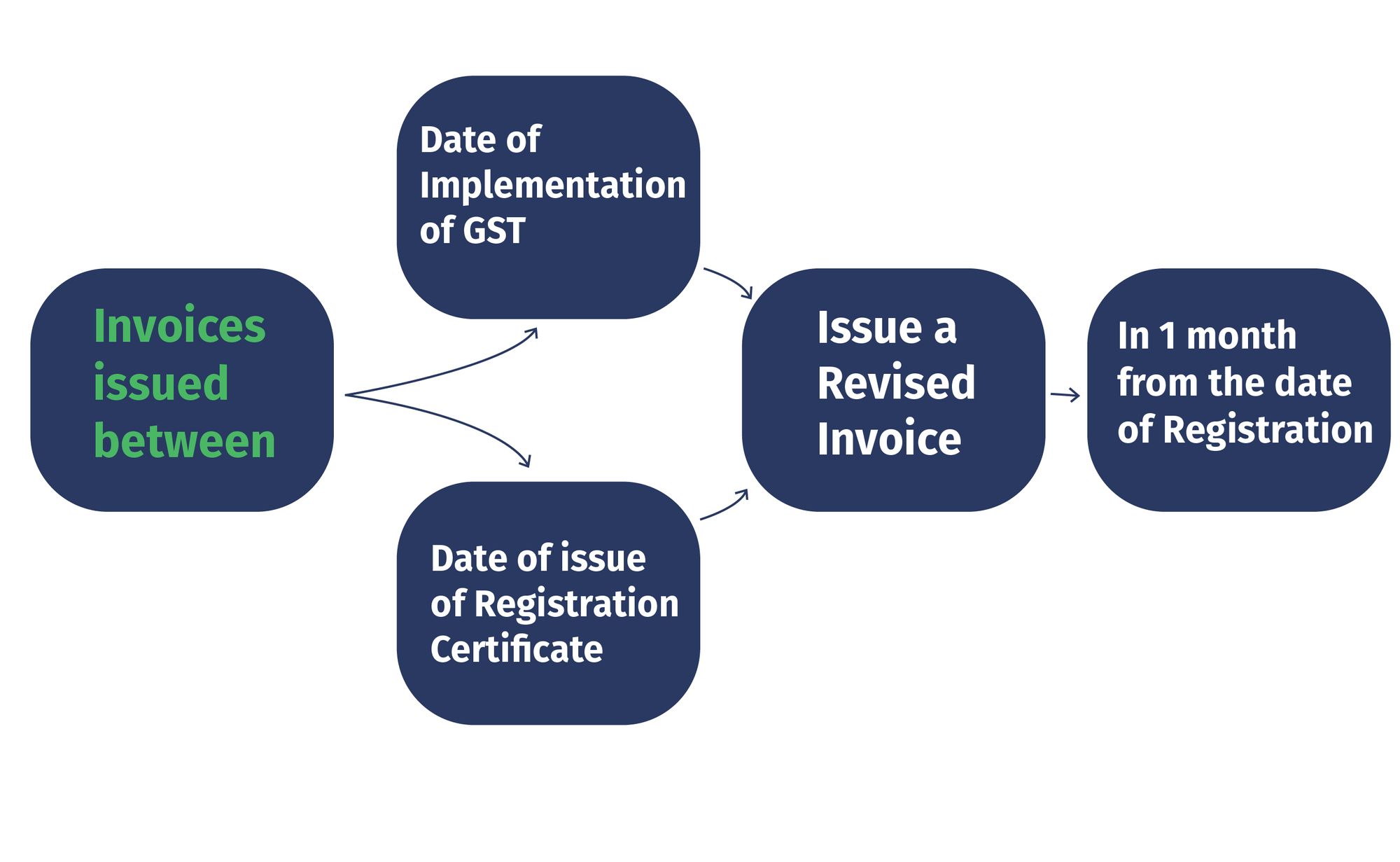

Can we revise invoices issued before GST?

You can revise invoices that were issued before the implementation of GST. However, you can only revise the invoice at intervals of one year from the date of supply, and also the revised invoices must comply with the GST law.

This image below can assist you to get a much better understanding of issuing a revised invoice:

This rule is applicable to all invoices generated between the day GST was implemented and the day your registration certificate was issued.

A corrected invoice must be issued by you as a dealer in relation to the previous invoices. The amended receipt must be given in no less than a multi-month from the date of issue of the enrollment declaration.

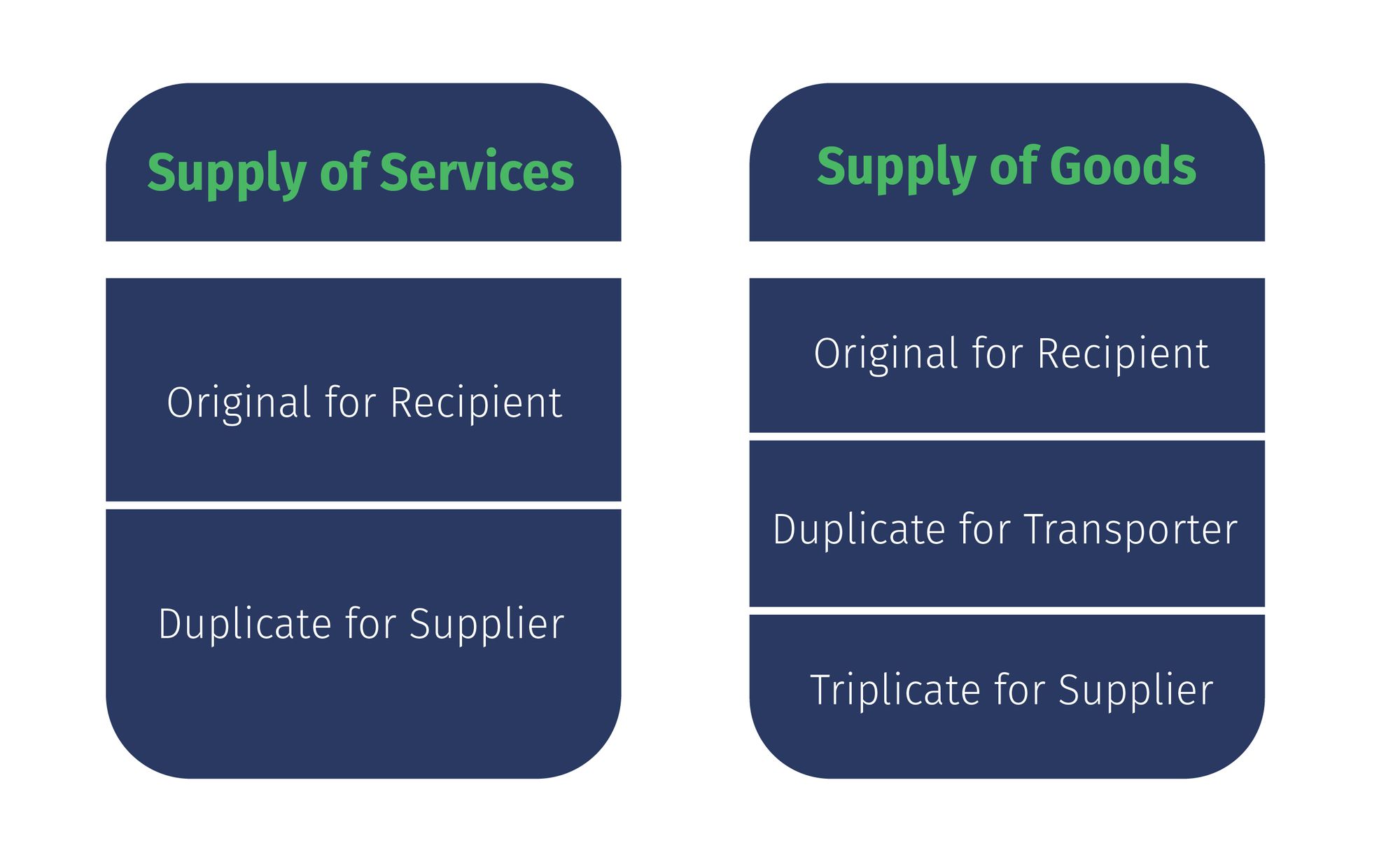

How many copies of Invoices Should We issue?

- For goods - 3 copies

- For services - 2 copies

GST Invoicing under Special Cases?

GST invoicing under special cases covers situations where the provider isn't registered under GST, situations where the provider is enrolled under GST, however, the beneficiary isn't, and situations where the stock is made to a unique financial zone.

There are a couple of extraordinary situations where the GST receipt rules are unique. These include:

1. When goods are sold on a consignment basis

2. When goods are sold through e-commerce websites

3. When Reverse Charge is applicable

4. When goods are sold to unregistered sellers

5. When the recipient pays GST

6. When two or more registered dealers exchange goods

7. When payments are received in advance for goods or services

8. When products are provided on a loan or hire purchase basis

9. When non-taxable services are provided

10. When unregistered service providers provide services

Get more information about GST Tax Invoices in Special Cases here.

What are the differences between tax invoices and delivery challan?

A tax invoice is produced by a registered provider for all taxable supplies of goods or services, as opposed to a delivery challan, which is primarily how they differ from one another. In contrast, a registered supplier must issue a delivery challan for any supply of goods or services, regardless of whether they are taxable or not.

The following information has to be on a tax invoice:

1. The supplier's name, address, and GSTIN.

2. A unique invoice number

3. A brief explanation of the goods or services supplied

4. HSN code of the goods or SAC code of the services

5. The volume of the goods or services supplied

6. The item or service's unit cost (inclusive of GST)

7. The whole worth of the products or services (inclusive of GST)

8. The GST rate

9. The GST charged amount

However, a delivery challan is not required to include all the information above, it must have the following details:

1. The supplier's name, address, and GSTIN.

2. A unique challan number

3. A brief description of the goods or services supplied

4. The amount of the products or services provided

5. The GST rate (if applicable)

6. The GST fee amount (if applicable)

More details regarding the distinctions between tax invoices and delivery challans can be found here.

FAQs on Tax Invoice in India

1. What is a GST Invoice?

A GST Tax Invoice could be a document that's issued by a GST-registered business to a different GST-registered company for the sale of taxable goods or services. It contains all the relevant sales transaction info, like the HSN code, description of goods or services, quantity, value, and GST rate.

2. What is included in GST Tax Invoice?

A GST Tax Invoice should include the following information:

· The name, address, and GSTIN of the provider

· A unique invoice number

· A date of supply

· The name, address, and GSTIN of the recipient

· An outline of the goods or services provided

· The HSN code of the goods or services

· The amount of the goods or services provided

· The unit value of the goods or services

· The whole price of the goods or services provided

· The GST rate

· The amount of GST charged

3. Types of GST Invoices

There are four varieties of GST invoices that may be issued by businesses, counting on the character of the transaction:

· Tax Invoice: A tax invoice is issued for the sale of taxable goods or services.

· Bill of Supply: A bill of supply is issued for the sale of exempt goods or services.

· Credit Note: A credit note is issued to regulate the worth of a taxable supply.

· Debit Note: A debit note is issued to change the worth of an excluded supply.

4. How to Create a GST Tax Invoice?

Accounting software like Kernel Finance can be used to create a GST Tax Invoice. Businesses can also construct a GST Tax Invoice using the GST Invoice Template.

5. Who should issue GST Invoice?

For the sale of taxable goods or services, a GST-registered firm is required to generate a GST Invoice.

6. By when you should issue invoices?

Invoices should be issued at intervals of 21 days from the date of the sypply of products or services.

7. Can you revise invoices issued before GST?

Yes, businesses will revise invoices that were issued before the introduction of GST. However, the revised invoice should contain the proper GST rate and also the correct GST quantity.

8. What are other types of invoices?

In addition to the four types of GST invoices, there are also 2 types of non-GST invoices:

· Tax Exempt Invoice: A nontaxable invoice issued for the sale of exempt goods or services.

· Bill of Entry: A bill of entry is issued for the import of goods into Republic of India.